There’s a special kind of anxiety that comes with large credit card debt. That moment when you look at the balance and can’t imagine ever seeing it at zero. Whether it’s $15,000, $30,000, or more, the size of your debt can feel paralyzing.

How to pay off large credit card debt is about breaking an overwhelming mountain into manageable steps.

Large debt follows the same principles as small debt, just on a different timeline. Understanding how to pay off large credit card debt means having a clear roadmap that takes you from “this feels impossible” to “I’m actually making progress.”

You don’t need to have all the answers right now. You just need to know the next right step. Let’s walk through this together, one move at a time.

Table Of Contents:

- Face the Numbers: Your First Step to Freedom

- Create a Realistic Budget You Can Stick To

- Pick a Debt Payoff Strategy: Snowball vs. Avalanche

- How to Pay Off Large Credit Card Debt Faster

- What if You Need More Help?

- Conclusion

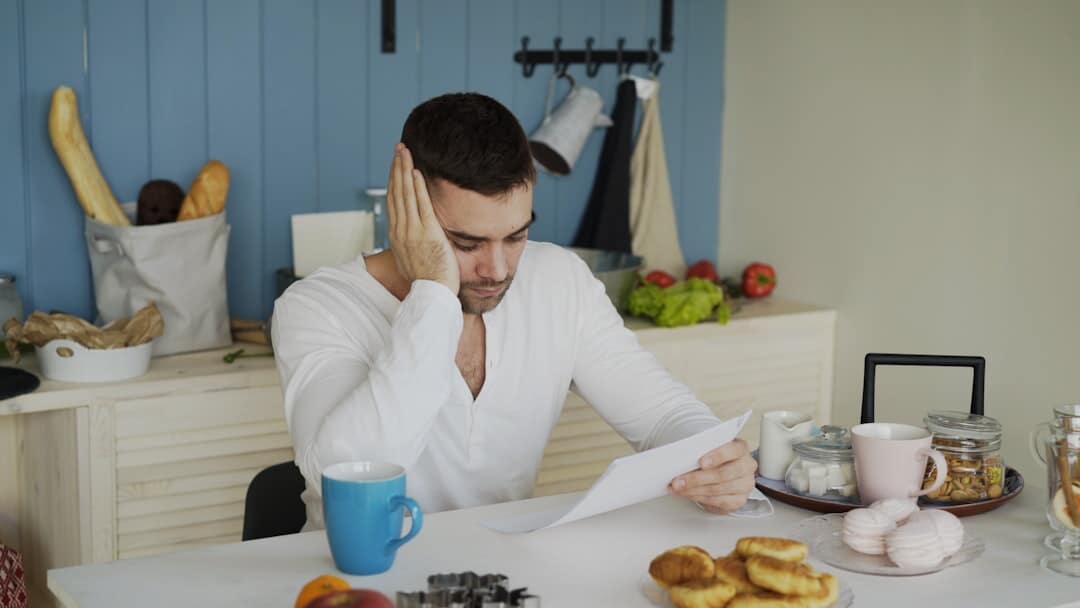

Face the Numbers: Your First Step to Freedom

Okay, this is the part nobody likes. But you can’t fight an enemy you can’t see. You have to know exactly what you are up against to make any real progress on the debt you’re carrying.

Take a deep breath and gather every credit card statement. Open a simple spreadsheet or grab a notebook. You need to list out every single debt you have to see the full picture of your financial situation.

For each card, write down three things: the total card balance, the annual percentage rate (APR), and the minimum monthly payment. Having this information organized is a powerful first step to getting your card pay plan in order.

Create a Realistic Budget You Can Stick To

The word “budget” makes a lot of people cringe. They think it means no more fun, ever. But that’s not true at all. Creating a budget is the key to changing your money habits.

A budget is just a plan for your money. It puts you in the driver’s seat. It shows you where your money goes, instead of wondering where it all went at the end of the month.

A great place to start is the 50/30/20 rule. The idea is to spend 50% of your after-tax income on needs, 30% on wants, and 20% on savings and debt reduction. It is a simple framework to get you going as you set goals for your finances.

Track Your Spending

To make a good plan, you need good information. This means you need to track your monthly expenses for about a month. This sounds tedious, but it is often an eye-opening experience that reveals where your money truly goes.

You can use an app that connects to your bank account or just use a small notebook. Write everything down, from your morning coffee to your rent. The goal is to see the real patterns in your spending habits.

Find Areas to Cut Back

Once you see where your money goes, you’ll spot places to cut back. You are not looking to slash and burn your lifestyle to the ground. You are looking for small, sustainable changes that free up cash for debt payments.

Maybe it is brewing coffee at home a few times a week instead of buying it. It could be canceling a streaming service you hardly watch or planning meals to reduce food waste. These little cuts add up to big dollars you can throw at your debt.

Pick a Debt Payoff Strategy: Snowball vs. Avalanche

Now that you have found some extra cash in your budget, you need a smart way to use it. Two of the most popular debt repayment methods are the debt snowball and the debt avalanche.

Your personality and what motivates you will help you decide which one is the right fit. One focuses on psychological wins to keep your motivation high. The other method is based on pure math to save you the most money on interest.

Both methods require you to pay at least the minimum payment on all your credit card accounts. The difference lies in where you direct any extra money you have.

| Feature | Debt Snowball | Debt Avalanche |

| Primary Focus | Paying off the smallest balance first. | Paying off the highest interest rate first. |

| Main Benefit | Quick motivational wins to keep you going. | Saves the most money on interest over time. |

| Best For | People who need to see fast progress to stay motivated. | People who want the most efficient, cost-effective plan. |

The Debt Snowball Method

The snowball method is all about building momentum. You focus all your extra money on your smallest balance first. You continue making just the minimum pay on everything else.

Once that smallest debt is gone, you celebrate that win. Then, you take the money you were paying on that debt and roll it over to the next smallest one. This creates a “snowball” of cash that grows as you knock out each debt.

This method works because those quick victories can give you the emotional boost you need to keep going for the long haul. Seeing a card with a zero balance credit can be incredibly encouraging.

The Debt Avalanche Method

If you are a numbers person, the debt avalanche might be for you. With this method, you attack the debt with the highest rate first. You still make minimum payments on all your other cards.

High interest is what keeps you in debt longer because the credit cards charge so much. By tackling the highest APR first, you pay less in total interest over the life of your debt. This is the most financially efficient way to get out of debt.

The avalanche method will always save you the most money. But, it might take a while to pay off that first big debt. You have to be patient and trust that the math is working in your favor.

How to Pay Off Large Credit Card Debt Faster

Following a budget and a payment schedule is a huge leap forward. But what if you want to speed things up? There are several ways to put your debt pay plan into overdrive.

This involves either bringing more money in or lowering the debt you pay. Doing both at the same time can drastically cut down your debt-free timeline. It takes work, but the results can be life-changing as you start paying off balances.

Increase Your Income

The fastest way to pay off debt is to make more money. Easier said than done, right? But it might be more possible than you think.

You might be in a position to ask for a raise at your job. Research your market value and present a strong case to your boss. Even a small increase can make a huge difference in your monthly debt payments.

Think about skills you already have. Could you do some freelance work on the side? You could also explore the gig economy with things like food delivery, ride-sharing, or dog walking to earn extra cash in your spare time.

Use Balance Transfer Cards

High interest rates are like trying to swim against a current. A balance transfer card can be a lifesaver. These cards offer a 0% introductory APR for a certain period, usually 12 to 21 months.

You can move your high-interest debt from your old cards to this new one. Now, your entire payment goes toward the principal, not interest. Be aware that most cards charge a transfer fee, typically 3% to 5% of the amount you move, and some may have an annual fee.

The key is to pay credit card debt off entirely before the introductory period ends. If you don’t plan carefully, the interest rate will jump up, often to a very high number.

You’ll need a good enough credit score to qualify for the best balance transfers.

Consider a Debt Consolidation Loan

If you have a lot of different card balances, a debt consolidation loan could help. This is a personal loan you use to pay off all your credit cards at once. You are left with just one monthly payment to the new lender.

Often, personal loans have much lower interest rates than credit cards. This can save you a lot of money and simplify your finances. This works best if you have a decent credit score to qualify for a good rate.

You can look for these loans at your local bank, credit union, or online lenders that specialize in debt consolidation loans. Just be sure to read all the terms, including any potential closing costs, before signing anything.

Improve Your Credit Utilization Ratio

An often-overlooked tool in your arsenal is your credit utilization ratio. This ratio is the amount of credit you’re using divided by your total available credit. Lenders look at this number to gauge how reliant you are on borrowed money.

A high utilization ratio can hurt your credit score, making it harder to qualify for things like a balance transfer card or debt consolidation loan. Generally, you want to keep this ratio below 30%. Paying down your card balances directly improves this ratio.

As you lower your credit utilization, your credit score should improve. A better score could help you refinance your debt at a lower rate, saving you even more money in the long run.

Contact Your Credit Card Company

Before you explore more drastic options, try a simple phone call. Contact each credit card company and ask if they can lower your interest rate. Explain that you’re committed to paying off your balance but the high interest is making it difficult.

Some creditors have hardship programs or may offer a temporary rate reduction. The worst they can say is no. A successful call could save you a significant amount of money and accelerate your debt pay journey.

What if You Need More Help?

Sometimes, even with the best plan, the debt is just too much to handle on your own. If you can’t pay your bills and feel like you’re drowning, it is time to ask for help. There is no shame in seeking professional guidance.

Credit counseling and debt resolution programs exist for this exact situation. A reputable debt resolution company can work with you to create a personalized plan. They have relationships with creditors and can often negotiate on your behalf to lower payment amounts.

The Consumer Financial Protection Bureau, a key agency for financial protection, advises consumers to research any company thoroughly. The goal is to find a legitimate organization that has your best interests at heart.

Credit Counseling and DMPs

A non-profit credit counseling agency can be a fantastic resource. A certified credit counselor will review your entire financial picture with you. They can help you create a workable budget and provide valuable financial education.

They might suggest a debt management plan (DMP). Under a DMP, you make one monthly payment to the counseling agency, and they distribute it to your creditors. Often, credit counselors can negotiate lower interest rates or waived fees, helping you pay off your debt faster than you could on your own.

Debt Settlement

Debt settlement is a more aggressive option and should be considered carefully. This process involves negotiating with a card company to pay a lump sum that is less than the full amount you owe. While it can resolve debt for a fraction of the cost, it can also have a serious negative impact on your credit score.

This path is usually for people who are severely behind on payments and see no other way out. It’s crucial to work with a reputable debt settlement firm and understand all the fees and consequences.

Avoid any company that asks for large upfront fees or makes promises that sound too good to be true.

Conclusion

You didn’t get into debt overnight, and you will not get out of it overnight either. But now you have a roadmap. From understanding your numbers to choosing a payoff strategy and exploring ways to accelerate your progress, you have the tools you need.

Remember to avoid common pitfalls like taking a cash advance from one card to pay another, as the fees and interest rates are typically astronomical. Focus on your plan and the positive changes you are making.

Be kind to yourself during this process. There will be good days and bad days. The important thing is to keep moving forward, one step at a time, until you are finally free. With a clear plan and persistence, you now know how to pay off large credit card debt and reclaim your financial freedom.

Debt won’t fix itself — but the right plan can. Use Simple Debt Solutions to compare multiple loan offers in one place and find the option that helps you pay less and get out of debt faster.