If you’re juggling multiple credit card payments with interest rates above 20%, you’re watching hundreds of dollars disappear into interest charges every month. Nearly half of credit card holders carry a balance, and 71 percent think they’ll pay off their balance within five years. But without a solid strategy, that timeline could stretch much longer.

Best debt consolidation companies offer a way out: combining your high-interest debts into a single payment, often at a fraction of your current interest rate. The average personal loan rate for debt consolidation is 11.66%, compared to the average credit card rate of 21.91%. That difference can save you thousands!

But not all debt consolidation companies are created equal. Some specialize in excellent credit borrowers, others work with fair or poor credit. Some offer lightning-fast funding, while others focus on the largest loan amounts. Finding the best debt consolidation companies means matching your credit profile and needs with the right lender.

Let’s break down the top options so you can make an informed choice.

Table Of Contents:

- Best Overall Debt Consolidation Companies for 2026

- Specialized Options Worth Considering

- How to Choose the Right Debt Consolidation Company

- When Debt Consolidation Loans Might Not Be the Best Choice

- Red Flags: Debt Consolidation Scams to Avoid

- The Application Process: What to Expect

- Take Control of Your Debt Today

Best Overall Debt Consolidation Companies for 2026

SoFi: Best Overall for Good to Excellent Credit

- APR Range: 8.99% – 29.99%

- Loan Amounts: $5,000 – $100,000

- Credit Score Required: 680+

- Funding Speed: 1-7 business days

SoFi’s personal loan is the best overall debt consolidation loan because it has a wide range of terms, doesn’t charge high mandatory fees, and offers decent APRs for borrowers with excellent credit.

What sets SoFi apart is its rate discount program: get 0.25% off for autopay, and another 0.25% off if you open a SoFi bank account with direct deposit of at least $1,000 monthly.

SoFi was ranked higher than the category average in the 2025 J.D. Power Consumer Lending Satisfaction Study, which means borrowers are consistently satisfied with their experience.

Best For: Borrowers with good to excellent credit who want competitive rates and no origination fees.

Upgrade: Best for Fair Credit

- APR Range: 7.74% – 35.99%

- Loan Amounts: $1,000 – $50,000

- Credit Score Required: 580+

- Funding Speed: 1-4 business days

Upgrade gives you the option of having the funds sent directly to credit card companies and other personal loan lenders, then sends excess loan amounts to your bank account. This direct payoff feature ensures your consolidation actually happens and you’re not tempted to spend the loan proceeds elsewhere.

The downside? Personal loans through Upgrade feature an origination fee of 1.85%-9.99%, which is deducted from the loan proceeds. But for borrowers with fair credit who struggle to get approved elsewhere, Upgrade’s accessibility makes it worth considering.

Best For: Borrowers with fair credit (580-679) who need direct creditor payoff and quick funding.

LightStream: Best for Large Loans

- APR Range: 7.49% – 25.99% (with autopay discount)

- Loan Amounts: $5,000 – $100,000

- Credit Score Required: 660+ (good to excellent credit preferred)

- Funding Speed: Same day to 1 business day

If you need up to $100,000 to consolidate large loan amounts like car, boat, and RV loans or want to zero out a home equity loan balance to sell your home, LightStream offers some of the lowest rates for high-dollar personal loans.

Even better: no fees and repayment terms up to seven years.

LightStream is a division of Truist Bank, so you’re working with an established financial institution rather than a fintech startup. More than 1 in 4 approved applicants qualify for the lowest available rate, making it competitive for well-qualified borrowers.

Best For: Borrowers with excellent credit who need large loan amounts and the lowest possible rates.

Discover: Best Low Rates for Qualified Borrowers

- APR Range: 7.99% – 24.99%

- Loan Amounts: $2,500 – $40,000

- Credit Score Required: 660+

- Funding Speed: 1-2 business days

Discover’s low interest rates, especially its highly competitive minimum APR of 7.99% for the most-qualified borrowers, make it a standout option. Discover also offers balance transfer credit cards as an alternative consolidation method, giving you flexibility in how you tackle your debt.

Discover gets high marks for customer satisfaction, coming in third in the 2025 J.D. Power Consumer Lending Satisfaction Study. You’re not just getting a good rate – you’re getting reliable customer service.

Best For: Borrowers with good to excellent credit who prioritize low rates and strong customer service.

Achieve: Best for Quick Approval and Funding

- APR Range: 7.99% – 35.99%

- Loan Amounts: $5,000 – $50,000

- Credit Score Required: 620+

- Funding Speed: 1-2 business days

Achieve is known for its quick approval and funding, making it ideal when you need to consolidate debt fast. While the APR range is wide, borrowers with fair to good credit can often secure competitive rates with available discounts.

Best For: Borrowers who need fast funding and have fair to good credit.

Specialized Options Worth Considering

Patelco Credit Union: Best for Credit Building

- APR Range: Starting at 7.99%

- Loan Amounts: Varies by membership

- Credit Score Required: 620+

- Unique Feature: LevelUp program

Patelco Credit Union offers a unique program that rewards you for on-time payments. Its “LevelUp” program allows you to lower your payment by up to 1.5 percentage points for every 12 months of on-time payments. This means your rate actually improves as you prove your reliability – a rare and valuable feature.

The catch? You need to become a member of the credit union first, but membership requirements are typically straightforward.

Best For: Borrowers who want their responsible payments rewarded with lower rates over time.

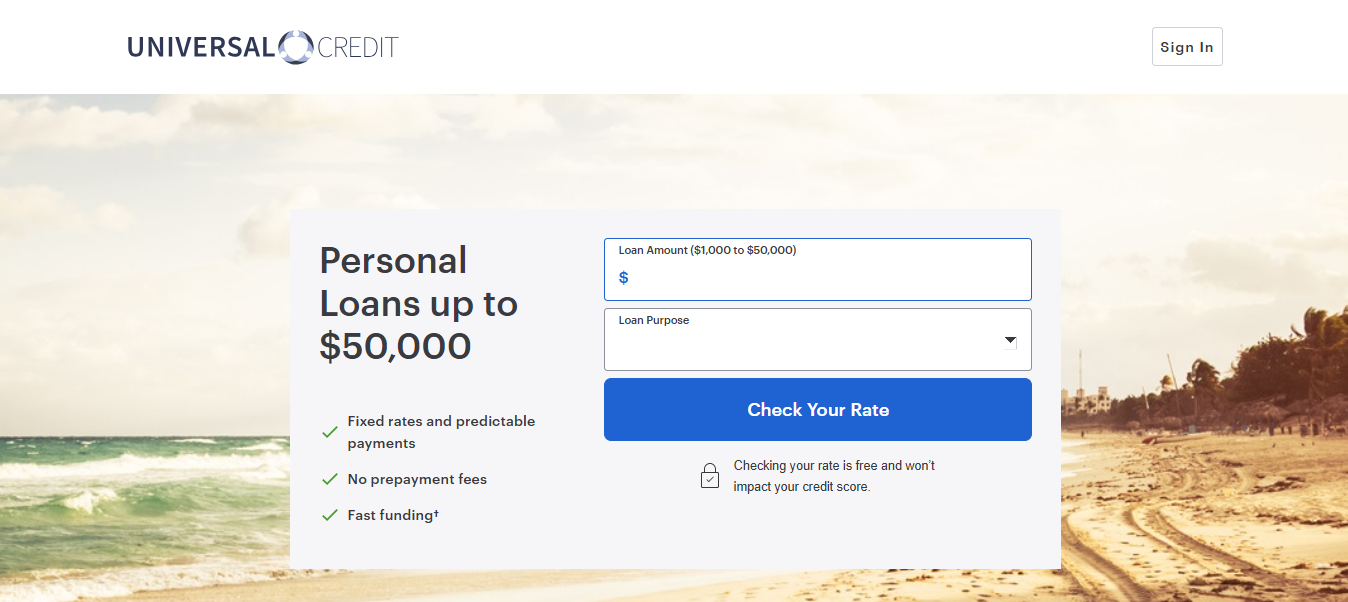

Universal Credit: Best for Bad Credit

- APR Range: 11.69% – 35.99%

- Loan Amounts: $1,000 – $50,000

- Credit Score Required: 560+

- Funding Speed: 1-4 business days

While people with excellent credit have their pick of lenders, there aren’t as many options out there for bad credit debt consolidation loans. Universal Credit fills this gap by accepting scores as low as 560, though you’ll face higher origination fees (5.25% – 9.99%).

Best For: Borrowers with poor credit who have been rejected by other lenders.

How to Choose the Right Debt Consolidation Company

1. Check Your Credit Score First

A quick check of your credit score gives you an idea of where you stand in terms of the credit brackets and which lenders may be the best fit based on their minimum credit score requirement.

Don’t waste time applying to lenders that won’t approve your credit profile.

2. Calculate Your Potential Savings

Look beyond the APR to see the total cost of the loan. A longer repayment term might lower your monthly payment but increase the total interest paid. Use this formula:

- Current total monthly payments × remaining months = Total cost without consolidation

- New monthly payment × loan term = Total cost with consolidation

- Compare the difference

3. Consider These Key Factors

- Compare rate (APR) ranges and run payment/interest math for your term.

- Note origination, late, prepayment, and annual fees.

- Check minimum credit score, DTI, and income requirements.

- Look for prequalification with a soft credit check.

- Check how quickly funds arrive and if direct-to-creditor payoff is available.

- Look for autopay, loyalty, or relationship rate discounts.

4. Prequalify with Multiple Lenders

Most lenders offer prequalification that won’t hurt your credit score. This lets you compare actual offers rather than advertised ranges. Getting 3-5 prequalifications gives you real negotiating power.

5. Read the Fine Print

Watch for:

- Origination fees that reduce your actual loan proceeds

- Prepayment penalties (though most lenders don’t charge these)

- Late payment fees

- Required autopay for the best rates

- Restrictions on how you can use the funds

When Debt Consolidation Loans Might Not Be the Best Choice

Before you consolidate, consider whether a loan is actually your best option:

Consider Credit Counseling Instead If:

Nonprofit consolidation is a payment program that combines all credit card debt into one monthly bill at a reduced interest rate and payment. These programs are offered by nonprofit credit counseling agencies that work with credit card companies to arrive at a lower, more affordable monthly payment.

This works when you have primarily credit card debt and would benefit from professional guidance alongside consolidation.

Try Balance Transfer Cards If:

A 0% intro rate card can pause interest for six to 21 months (balance transfer fee is usually 3% to 5%). It works best if you can pay off the entire balance before the promo ends and avoid new purchases.

This is ideal when you can realistically pay off your debt within 12-21 months and have good enough credit to qualify for promotional rates.

Consider Debt Settlement If:

Debt settlement involves negotiating with creditors to accept less than the full amount owed, typically 40-60% of your original balance. This option might make sense if:

- You’re severely behind on payments and facing collections or lawsuits

- You cannot afford the minimum payments even after consolidation

- You’re considering bankruptcy as your only other option

- You have a lump sum available to offer creditors

Warning: Debt settlement severely damages your credit score for up to seven years. Settled accounts are marked on your credit report, creditors may send 1099-C forms for “forgiven” debt (which counts as taxable income), and you’ll face collections calls during the negotiation period. Only consider this as a last resort before bankruptcy.

Red Flags: Debt Consolidation Scams to Avoid

Keep your guard up against credit repair scams that promise results that don’t seem possible. There are plenty of advertisements in this industry that sound too good to be true … and it’s because they are.

Watch out for companies that:

- Guarantee they can eliminate your debt for pennies on the dollar

- Charge large upfront fees before providing any services

- Tell you to stop communicating with your creditors

- Promise to “erase” bad credit or create a new credit identity

- Aren’t transparent about fees and terms

- Pressure you to sign immediately without reviewing the terms

Legitimate lenders allow prequalification, clearly disclose all fees, and give you time to review loan agreements.

The Application Process: What to Expect

Step 1: Prequalify

Submit basic information to multiple lenders to see estimated rates without affecting your credit score. This soft inquiry shows you what you’re likely to be offered.

Step 2: Compare Offers

Look at APR, monthly payment, total interest cost, fees, and repayment terms. The lowest APR isn’t always the best deal if fees are excessive or the term is too long.

Step 3: Formally Apply

Once you choose a lender, complete the full application. You’ll need:

- Proof of identity (driver’s license, passport)

- Social Security number

- Proof of income (pay stubs, tax returns, bank statements)

- Employment information

- Current debt information

This triggers a hard credit inquiry, which temporarily lowers your credit score by a few points.

Step 4: Review and Accept Loan Terms

Be sure the new monthly payments do not impact your ability to cover your basic living expenses first, and factor in any fees you have to pay.

Read everything carefully. Make sure you understand the payment due date, how interest is calculated, and any conditions for rate discounts.

Step 5: Receive Funds and Pay Off Debts

Some lenders may offer to send the loan funds to your creditors for you, so you’ll need to provide the correct account information. This direct payoff option removes temptation and ensures consolidation actually happens.

If funds come to you, immediately pay off your credit cards and other debts. Keep confirmation of each payoff.

Take Control of Your Debt Today

Comparing the best debt consolidation companies gives you the power to escape the high-interest trap. Whether you have excellent credit and qualify for the lowest rates, or you’re rebuilding and need a lender willing to work with fair credit, there’s an option that can save you money.

The credit card companies are counting on you to keep making minimum payments while they collect maximum interest. Debt consolidation flips that script: you get a clear payoff date, lower interest, and one simple payment to manage.

If you’re carrying over $20,000 in high-interest credit card debt, Simple Debt Solutions can help you evaluate your consolidation options and find the right lender for your situation. We’ll help you understand your choices, compare real offers, and create a plan to become debt-free faster while saving thousands in interest.

Stop letting high interest rates steal your financial future. Start your debt consolidation journey today.